Voluntary Carbon Market Outlook

Download the Full VCM Analysis

The voluntary carbon market didn’t shrink. It got more selective. See what four years of retirement data reveals about where buyer confidence is.

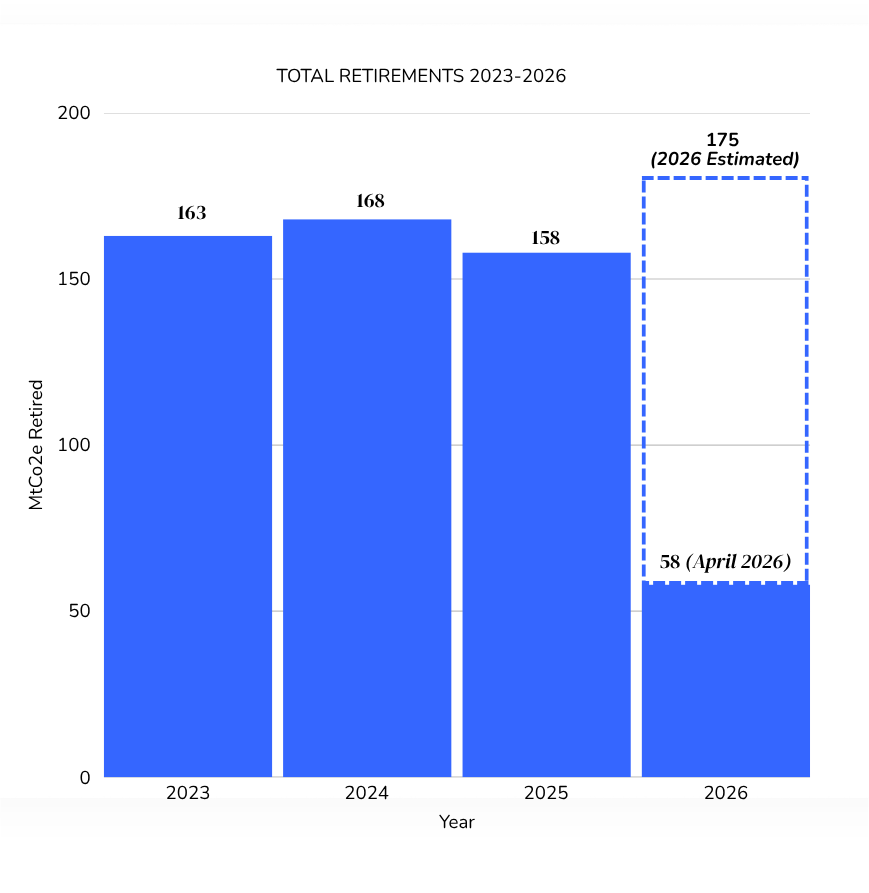

Retirement volumes in the voluntary carbon market have held broadly stable since 2023. What has shifted is what buyers are willing to retire, and why. CarbonBetter analyzed four years of data to find out.

The Voluntary Carbon Market has evolved and matured substantially since its inception roughly 20 years ago. What began as a relatively niche way for companies to support climate projects has become a more structured market, shaped by corporate climate commitments, independent standards bodies, registries, ratings providers, and growing expectations around credit quality.

Buyers have become more selective. Scrutiny over credit quality has intensified. And the project types that are gaining share are the ones that can withstand harder questions.

CarbonBetter analyzed retirement data from the Berkeley Voluntary Registry Offsets Database (BVROD) to understand what market behavior over this period reveals about the direction of the VCM. We break down retirement trends by project type, examine the forces reshaping buyer behavior, and identify what the data suggests about where the market is headed next.

Big Picture

Retirement volumes have been broadly stable over the period shown. But volume alone does not tell the full story. What has shifted is not how much is being retired, but what is being retired and why. The following sections break down retirements by project type, where the more telling trends emerge.

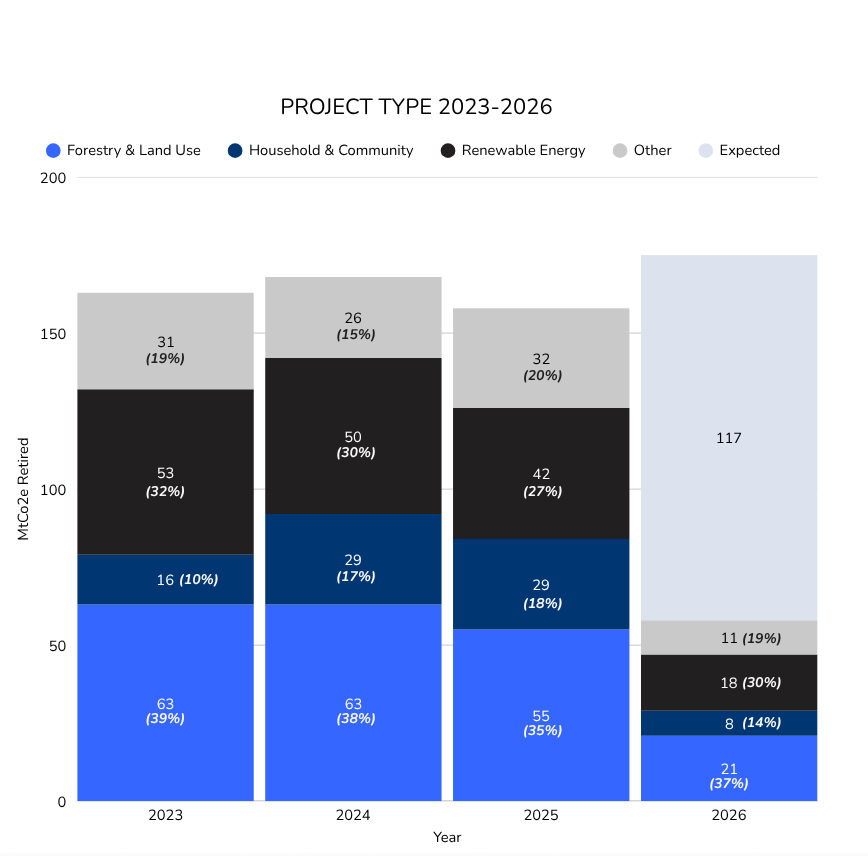

Project Type

Retirements point to a more selective market

- Forestry & Land Use has remained the largest project type across the period, but its share of total retirements has edged downward. Volume held flat from 2023 to 2024, then fell in 2025. The decline reflects growing buyer selectivity about which projects within the category they are willing to retire.

- Renewable Energy has declined in absolute terms each of the past three years. The driver is structural: as wind and solar became commercially viable in most markets, credits became harder to defend as genuinely additional emissions reductions. The Integrity Council for the Voluntary Carbon Market (ICVCM) formalized that concern in August 2024, and the retirement trend suggests buyers had already begun moving away before the ruling.

- Household & Community is the only category that grew, nearly doubling from 2023 to 2024 and holding that level through 2025, even as the overall market fell. Projects in this category have proven resilient because they offer something many credit types cannot: a co-benefit (any positive social, economic, or environmental impact that a climate project generates in addition to its primary goal) story that is tangible and easy to communicate with external stakeholders.

Additionality of Carbon Offset Projects

Gain a deeper understanding of additionality in carbon offset projects, empowering you to make well-informed decisions when purchasing carbon credits.

Forestry & Land Use

Reducing Emissions from Deforestation and Forest Degradation (REDD+) projects are among the most widely issued credit types in the voluntary carbon market, the majority of which were registered under Verra, the market’s largest standards body. The 2023 credibility crisis changed REDD+ permanently. A Guardian investigation challenged Verra’s crediting system, and Bloomberg’s reporting on the Kariba project revealed that over half of its ~27 million credits were likely issued in excess, a finding Verra’s own review confirmed. For corporate buyers already under pressure over nature-based offsets, REDD+ became hard to defend. Retirements have fallen every year since.

It hasn’t disappeared, though. Early 2026 data shows activity consolidating around a small number of high-credibility projects, a “smaller and sharper” market, not a recovery.

Improved Forest Management (IFM) projects focus on managed forests; adjusting practices such as harvest rotations, reduced-impact logging, or converting timber land to conservation. These absorbed some of the shift, with retirements roughly doubling by 2025. But growth was concentrated in a handful of projects, and formal integrity certification for the category only arrived in December 2025. Buyers rotated in before any quality stamp existed.

Renewable Energy

As wind and solar became more commercially viable without carbon finance, concerns about the additionality have put downward pressure on this category. The ICVCM made it official in August 2024, ruling that eight renewable energy methodologies couldn’t receive the Core Carbon Principles label due to weak additionality standards. Around 236 million unretired credits, roughly 32% of issued and unretired credits of the voluntary carbon market, were affected. Buyer behavior shifted noticeably in 2025.

Wind has held up better than solar or hydro, likely because projects in emerging markets retain a more credible additionality case. But the direction for the category is clear: as the cost structure for renewable energy projects shifts, it reasonable to be concerned about additionality concerns going forward.

Early data for 2026 might indicate durable demand. Data through April already shows 19 Mt CO2e retired, which, if historical seasonality holds, implies a full-year figure that would make 2026 the highest retirement year on record for Renewables. It’s too early to draw conclusions, and the pattern may not hold. But it’s a finding we’re actively monitoring.

Household & Community

Cookstoves dominate Household & Community retirements, with clean water the next most significant subtype. The appeal starts with co-benefits: cleaner air, safer water, reduced energy costs, and time savings for women and children, impacts that extend well beyond carbon accounting. What reinforces that appeal is how visible those impacts are. A stove is installed, a household burns less fuel, a water filter removes the need to boil water. In a market where buyers increasingly need to explain their climate investments to customers, auditors, and the media, that directness matters.

That durability has limits, though. Cookstove credits have faced scrutiny over baseline assumptions, over-crediting, and real-world adoption rates. In March 2025, the ICVCM approved three cookstove methodologies for CCP eligibility while rejecting two others for weak measurement standards. The approvals came with conditions expected to reduce credits issued per project going forward.

This is not a uniform quality category. The ICVCM decisions have put those concerns as priority for most buyers.

Overarching Themes in VCM

- Quality now drives demand. Buyers are no longer treating credits as interchangeable; additionality, monitoring, permanence, and methodology approval are shaping retirements.

- Demand is shifting across project types. Total retirements moved unevenly from 2023 to Q1 2026, but the more important story is reallocation. Forestry and Land Use remain large, but buyers are sorting REDD+, Improved Forest Management, and Afforestation/Reforestation differently. Renewable Energy is losing ground as older methodologies fail additionality tests. Household and Community projects are gaining share because they offer tangible interventions and visible co-benefits.

- It’s not only an environmental story, it’s a social one too. The growth of Household and Community projects points to something broader than a preference for a particular project type. Buyers are increasingly drawn to credits that deliver visible, human outcomes alongside emissions reductions. In a market where companies face growing scrutiny over what they can publicly defend, co-benefits have moved from a nice-to-have to a real purchasing signal. The credits that are gaining ground are the ones that can tell a story beyond the carbon reduction.

The shift in buyer behavior documented here has real implications for any organization with carbon credits in its climate strategy. Download the full report for the complete data, project-level detail, and the analysis behind each finding.

Download the Full VCM Analysis

The voluntary carbon market didn’t shrink. It got more selective. See what four years of retirement data reveals about where buyer confidence is.

Read More on Carbon Credits

Carbon Credit Lifecycle

Explore the multi-step lifecycle of carbon credits, designed to deliver credible, transparent, and third-party verified climate benefits, helping you achieve your sustainability goals.

Additionality of Carbon Offset Projects

Gain a deeper understanding of additionality in carbon offset projects, empowering you to make well-informed decisions when purchasing carbon credits.

Criteria for High-Quality Carbon Credits

Comparing rating systems vs. protocols and defining top criteria to empower businesses with the knowledge to assess high-quality carbon credits.