What Are Scope 3 Emissions?

Closing the Carbon Market Gap

According to Bank of America, carbon offset supply may need to grow as much as 50x by 2050 to achieve net-zero emissions. Watch the replay as three experts discuss efforts to close this gap and the challenges in developing projects and issuing credits at scale.

Unpacking Scope 3 carbon emissions by first defining what Scope 3 emissions are, with examples, then sharing three ways to manage these indirect emissions.

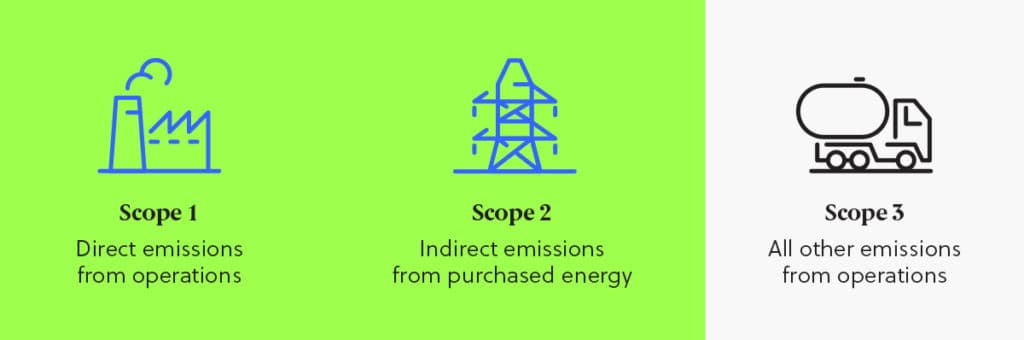

Carbon emissions classification often comes in three major scopes—Scope 1, 2, and 3—each reflecting a different level of organizational influence and control over greenhouse gas (GHG) emissions. Scope 1 and 2 emissions are typically easier to quantify, largely representing an organization’s direct emissions from fossil fuel combustion and indirect emissions from purchased electricity, respectively. However, depending on the complexity of a company and its supply chain, the majority of a company’s carbon footprint can stem from Scope 3 emissions. These emissions are generated from all other indirect sources that occur due to an organization’s activities but originate from sources not owned or controlled by the organization. Understanding and accounting for Scope 3 emissions, and then ultimately reducing Scope 3 emissions, are crucial steps for businesses aspiring to develop a comprehensive sustainability program.

Scope 3 Emissions: A Deeper Look

Scope 3 emissions encompass a broad range of activities that aren’t directly owned or controlled by an organization. In its guidance for quantifying Scope 3 emissions, the GHG Protocol groups Scope 3 emissions into 15 distinct categories.

Here’s a brief definition of each category:

- Purchased goods and services: Emissions from the production of goods and services bought by the company.

- Capital goods: Emissions from the life-cycle of long-term goods (e.g., machinery, buildings).

- Fuel-and energy-related activities: Emissions linked to the production of fuels and energy purchased by the company, not included in Scope 1 or 2.

- Upstream transportation and distribution: Emissions from the transportation and storage of goods and materials purchased by the company, but transported by a third party.

- Waste generated in operations: Emissions from disposal and treatment of waste generated by the company’s operations.

- Business travel: Emissions from business travel undertaken by employees in vehicles not owned or controlled by the company.

- Employee commuting: Emissions from employees commuting to and from work.

- Upstream leased assets: Emissions from leased assets that the company doesn’t directly control or operate.

- Downstream transportation and distribution: Emissions from the transportation, storage, and delivery of goods sold by the company, where this transportation is not controlled by the company.

- Processing of sold products: Emissions arising from the processing of goods sold by the company (e.g., cooking of food sold by a retailer).

- Use of sold products: Emissions from the use of goods and services sold by the company.

- End-of-life treatment of sold products: Emissions from the disposal and treatment of goods sold by the company when those goods reach their end-of-life stage.

- Downstream leased assets: Emissions from the operation of assets leased out by the company.

- Franchises: Emissions from franchisees’ operations.

- Investments: Emissions from the operation of investments not owned or controlled by the reporting company, but for which the company has financial investment.

To dig deeper into some specific areas, we have explored what potential emissions sources would be included in the following example categories:

Potential Scope 3 Emissions Examples

| Scope 3 Category | Description | Example |

| Supply Chain and Logistics | Emissions from the manufacture of inputs and transportation are often significant, especially for manufacturing and retail companies. | A fashion retailer would account for emissions from the farming of cotton, the production of synthetic materials, and the shipping of raw materials and final products. |

| Corporate Travel | Emissions from business-related travel using vehicles not owned or controlled by the reporting entity. | Emissions from an employee flying across the country for a business meeting. |

| Work From Home | Employees commuting from home and using energy for work-related tasks could generate substantial emissions over time. | An employee using their personal computer and electricity to work from home. |

Skip the RFP—CarbonBetter can help

CarbonBetter Certified Offset Portfolios allow carbon buyers to participate in a variety of projects, geographies, and technologies in one simple transaction rather than navigating a lengthy and complex RFP process with multiple carbon market participants.

Learn More about CBCO 22-1Understanding and accurately categorizing and then quantifying the carbon from each of these emissions sources is important for an organization aiming to develop a comprehensive GHG accounting program across Scopes 1, 2, and 3. It not only ensures correct reporting and accurate disclosures but also helps in identifying significant sources of emissions, thereby informing effective mitigation strategies to reduce Scope 3 emissions.

Supply chains, in particular, can add a level of complexity to Scope 3 carbon emissions accounting. Consider the different tiers of suppliers: Tier I suppliers, who directly supply to the company; Tier II suppliers who supply to Tier I suppliers; and Tier III suppliers, who supply to Tier II suppliers. Each supplier within each tier can have its unique emissions profile, contributing to the overall Scope 3 emissions of an organization. Understanding this structure and how emissions propagate through the supply chain can prove challenging but is important in guiding effective strategies for emissions reduction.

Scope 3 Emissions: A Spend-Based Perspective

While the vastness of Scope 3 emissions can be overwhelming, a useful starting point for many companies is a spend-based perspective. This involves looking at procurement and purchasing decisions and evaluating GHG emissions associated with financial transactions, with a focus on its largest spending categories. For instance, a company that spends a large portion of its budget on air travel will likely find that this is a significant source of Scope 3 emissions.

However, while a spend-based approach can help highlight potential areas of significant emissions, it is not without its challenges. Estimates derived from this method tend to be rough and lack accuracy due to the broad assumptions made about GHG emission factors. Thus, they should serve as a tool for initial identification and subsequent detailed evaluation rather than a definitive quantification of emissions.

The Life Cycle Informed Approach

The life cycle-informed approach offers a more comprehensive perspective on Scope 3 emissions. It considers the emissions from all stages of a product or service's life cycle, from raw material extraction through materials processing, manufacturing, distribution, use, repair and maintenance, and disposal or recycling.

This approach can unveil less obvious but substantial sources of emissions that a spend-based approach might overlook. It also promotes a broader understanding of a product or service’s environmental impact, informing more strategic and impactful mitigation measures.

Supplier Specific Data

Diving deeper into the complexities of Scope 3 emissions, we find that supplier engagement plays a significant role, particularly in industries with complex supply chains. Therefore, implementing a supplier-specific approach is a robust strategy for managing Scope 3 emissions.

For example, supplier questionnaires can be a powerful tool for gathering data about suppliers' GHG emissions, environmental practices, and sustainability strategies. This approach enables an organization to quantify Scope 3 emissions accurately and helps identify potential areas for improvement and collaboration. This information can help companies create a comprehensive emissions profile, leading to more accurate tracking and better decision-making processes.

Integrating the emissions contributions from Tier I, II, and III suppliers into this discussion reveals an intricate web of relationships and emission sources that define Scope 3 emissions. Navigating complex supplier relationships, understanding the unique emissions profile from suppliers across each tier, and incorporating this data into carbon accounting practices can significantly enhance the accuracy and reliability of your Scope 3 emissions management.

Conclusion

Accurately assessing and managing Scope 3 emissions requires a plan, stakeholder engagement, and significant volumes of data, which may feel overwhelming for many organizations. CarbonBetter offers support to ensure the proper implementation of GHG accounting methodologies, the correct categorization of emissions, and the establishment of repeatable processes for accuracy year after year. Don't tackle the complexities of Scope 3 emissions alone; we are here to help wherever you are in your sustainability journey. Contact us today to get started.

Scope 1 emissions are direct emissions that come from sources owned or controlled by an organization, such as emissions from company-owned vehicles or buildings. Scope 2 emissions are indirect emissions from the generation of purchased electricity or purchased steam, heat and cooling consumed by the company. Scope 3 emissions, on the other hand, are all other indirect emissions that occur in the value chain of the reporting company, including both upstream and downstream emissions.

Calculating Scope 3 emissions can be challenging because it involves understanding emissions that occur from sources not owned or controlled by the organization. These emissions are typically influenced by the actions of suppliers, customers, or other stakeholders in the value chain. This requires gathering data from a variety of sources, which can be time-consuming and complicated.

Companies can reduce their Scope 3 emissions by implementing sustainability practices across their value chain. This could include choosing suppliers with lower carbon footprints, reducing business travel, promoting remote work, and encouraging customers to use their products or services in more sustainable ways. Working with suppliers to improve their sustainability practices can also be a powerful way to reduce Scope 3 emissions.

Managing Scope 3 emissions can help businesses identify risks and opportunities within their value chain, improve efficiency, drive innovation, enhance brand reputation, and meet regulatory and customer expectations. In addition, a comprehensive understanding of Scope 3 emissions can support strategic decision-making and planning, leading to competitive advantage.

CarbonBetter can help businesses understand, measure, and reduce their Scope 3 emissions. Our team can provide support at all stages of your sustainability journey, from conducting a detailed Scope 3 emissions assessment to developing and implementing a strategic plan for emissions reduction. Contact us today to get started.

About the Author

Pankaj Tanwar is Managing Director of Climate Services at CarbonBetter. He has experience leading Fortune 100 companies through their sustainability journeys, including sustainability driven growth in the food industry. Pankaj holds an MBA from Northwestern University’s Kellogg School of Management and a BTech in Mechanical Engineering from the Indian Institute of Technology, Kanpur.

From the Stories

Edition #6 | Your Sustainability Team’s Weekly Briefing

Welcome to your weekly sustainability briefing! We're covering three developments that are reshaping how businesses think about climate risk, carbon markets, and the politics of the green transition.

Edition #5 | Your Sustainability Team’s Weekly Briefing

Welcome to your weekly sustainability briefing! We're covering three developments that are reshaping how businesses think about climate risk, carbon markets, and the politics of the green transition.

Edition #4 | Your Sustainability Team’s Weekly Briefing

Welcome to your weekly sustainability briefing! We're covering three developments that are reshaping how businesses think about climate risk, carbon markets, and the politics of the green transition.